Equinox Gold Corp. (TSX-V: EQX, OTC: EQXGF) (“Equinox Gold” or the “Company”) is pleased to announce the results of the prefeasibility study (“PFS”) for its 100% owned Castle Mountain Gold Mine (“Castle Mountain” or the “Project”) located in California, USA. The PFS contemplates a low-cost heap leach gold mine with 3.6 million ounces (“oz”) of gold reserves that will produce 2.8 million oz of gold and generate $865 million in after-tax cash flow over a 16-year mine life.

Castle Mountain will be developed in two phases with annual average gold production of 45,000 oz over the first three years (“Phase 1”) and annual average gold production of 203,000 oz from years 4 to 16 (“Phase 2”). With Measured & Indicated Mineral Resources estimated at 4.3 million oz of gold (inclusive of reserves), Inferred Mineral Resources of 2.2 million oz and additional near-mine mineralization identified with the 2017 exploration program, there remains potential to extend the mine life and increase annual production.

All amounts are in US dollars unless otherwise indicated. Base case economics were calculated using a $1,250/oz gold price. The Company will host a webcast and conference call at 8:00am PT (11:00am ET) on July 17, 2018 to present the PFS results. Further details are provided at the end of this news release.

PFS HIGHLIGHTS

- 3.6 million oz of Proven & Probable Mineral Reserves grading 0.56 grams per tonne (“g/t”) gold

- $865 million after-tax life of mine (“LOM”) cumulative cash flow

- $763/oz average LOM all-in sustaining costs (“AISC”)

- 2.8 million oz LOM gold production

- 45,000 oz average annual gold production during Phase 1 (years 1-3)

- 203,000 oz average annual gold production during Phase 2 (years 4-16)

- $406 million after-tax net present value discounted at 5% (“NPV5%”) ($534 million at $1,350/oz gold)

- 20% internal rate of return (“IRR”) (25% at $1,350/oz gold)

- Phase 1 capital costs of $52 million and Phase 2 capital costs of $295 million with LOM sustaining capital costs of $142 million

- Phase 1 ore stacking and commissioning targeted for end of 2019

- Initial 16-year mine life with expansion potential from existing near-mine mineralization

Christian Milau, CEO of Equinox Gold, stated: “The prefeasibility study contemplates a robust, long-life, high-margin gold mine in an excellent mining jurisdiction that will generate significant gold production and cash flow for Equinox Gold shareholders. Castle Mountain increases the Company’s gold reserves by more than 350% to 4.5 million ounces while significantly increasing future annual gold production. Combined production from the Aurizona and Castle Mountain mines will total almost 200,000 ounces of gold by 2020 and increase to 350,000 ounces, with all-in costs in the lowest quartile of the industry and significant expansion upside from both mines.”

Ross Beaty, Chairman of Equinox Gold, stated: “Castle Mountain is Equinox Gold’s second cornerstone mine that, by itself, will generate more than one billion dollars of pre-tax cash flow at current gold prices. Successful execution of mine development at both Aurizona and Castle Mountain will establish Equinox Gold as a mid-tier gold producer. We have the operating team in place to rapidly advance these mines while our exploration team demonstrates the great geologic potential at both projects to further enhance the value of these assets for our shareholders.”

OVERVIEW

The Castle Mountain Gold Mine, located in San Bernardino County, California, produced more than one million oz of gold as an open-pit heap-leach mine from 1992 to 2004, when production ceased due to low gold prices and the mine was substantially reclaimed. Under the PFS mine plan, Phase 1 of the Project will produce for three years with average annual production of 45,000 oz of gold. Phase 2 production is expected to average 203,000 oz of gold annually for 13 years, for total LOM production of 2.8 million oz. LOM AISC are estimated at $763/oz, which is in the lowest quartile of the industry. The Project demonstrates strong returns with an after-tax NPV5% of $406 million and an after-tax IRR of 20% using the base case gold price of $1,250/oz ($534 million and 25% at $1,350/oz gold price). The Project is expected to generate average annual after-tax net operating cash flow of $83 million with cumulative LOM after-tax net cash flow of $865 million. At $1,350/oz gold, the Project would average more than $96 million in after-tax net operating cash flow annually and generate more than $1 billion in cumulative after-tax net cash flow over the 16-year mine life.

PFS Highlights 1

| Phase 1 (yrs 1-3) | Phase 2 (yrs 4-16) | Total Project | |

| Gold Price | $1,250 oz | ||

| Ore | 197.6 M tonnes | ||

| Grade | 0.35 g/t (ROM) | 0.43 g/t (ROM) 3.23 g/t (mill) | 0.56 g/t |

| P&P Reserve | 3,563,093 oz | ||

| Average annual production | 44,930 oz | 202,979 oz | 173,345 oz |

| Recoverable LOM gold | 2,798,173 oz | ||

| Throughput | 12,700 tpd | 41,000 tpd | |

| Strip ratio | 3.6 | ||

| Recovery | 72% (ROM) | 72% (ROM) 94% (mill) | 79% |

| Mine life | 3 | 13 | 16 |

| Initial capex 2 | $52 M | $295 M | $347 M |

| Sustaining capex 3 | $142 M | ||

| Cash cost (including royalties) | $889/oz | $703/oz | $712/oz |

| AISC | $980/oz | $752/oz | $763/oz |

| Pre-tax NPV 0% | $1,034 M | ||

| Pre-tax NPV 5% | $491 M | ||

| Pre-tax IRR | 21.7% | ||

| After-tax NPV 0% | $865 M | ||

| After-tax NPV 5% | $406 M | ||

| After-tax IRR | 20.1% | ||

| After-tax average annual operating cash flow 4 | $16 M | $99 M | $83 M |

1. PFS estimates are considered accurate +/- 20%. 2. Includes working capital and contingency. 3. Includes $20.2 million of reclamation/closure costs and contingency. 4. Undiscounted.

Castle Mountain has the key permits and the water supply required to commence Phase 1 production, with a Conditional Use Permit (“CUP”), Reclamation Plan and a valid Record of Decision (“ROD”) to mine up to 46,600 tonnes per day (“tpd”) of ore plus waste. Phase 1 will consist of a run-of-mine (“ROM”) heap leach operation processing primarily 12,700 tpd of stockpiled ore from previous operations. Phase 2 will increase throughput to 41,000 tpd of ore, of which 2,340 tpd of higher-grade ore will be processed through a milling circuit. The phased ramp-up approach allows the Company to use existing permits to expedite production while completing the feasibility study and permitting for the Phase 2 expansion. While Phase 2 will operate within the existing permitted mine boundary, the increased mining and water extraction rates will require updated permitting for the Project.

ECONOMIC SENSITIVITIES

Using the base case gold price of $1,250/oz and incorporating only Proven and Probable Mineral Reserves of 3.6 million oz of gold, the Project has an after-tax NPV5% of $406 million and an after-tax IRR of 20%. The Project’s economics are most sensitive to fluctuations in the gold price, as summarized in the tables below.

Castle Mountain Mine Sensitivity to Gold Price

| Gold price ($/oz) | $1,150 | $1,250 | $1,350 |

| NPV5% (after tax) | $276.4 M | $406.5 M | $534.2 M |

| IRR (after tax) | 15.2% | 20.1% | 25.1% |

Castle Mountain Mine Sensitivity to Capital Costs

| Capital costs 1 | -10% | $471.0 M | +10% |

| NPV5% (after tax) | $435.6 M | $406.5 M | $377.5 M |

| IRR (after tax) | 22.5% | 20.1% | 18.1% |

1. Includes sustaining capital and recapture of $18 million of working capital at end of mine life.

Castle Mountain Mine Sensitivity to Operating Costs

| Operating costs | -10% | $1,836.0 M | +10% |

| NPV5% (after tax) | $495.2 M | $406.5 M | $315.6 M |

| IRR (after tax) | 24.0% | 20.1% | 16.4% |

CAPITAL & OPERATING COSTS

Initial capital for Phase 1 construction is estimated at $52 million, with many aspects of the Phase 2 expansion incorporated into the design to reduce total LOM capital costs. Initial capital for Phase 2 construction is estimated at $295 million, including $47 million in capitalized pre-stripping. Cost estimates are summarized in the tables below.

Castle Mountain Capital Cost Estimates

| Cost Area | Phase 1 Capital (M$) | Phase 2 Capital (M$) | Sustaining Capital (M$) |

| Mine equipment | 1.4 | 111.5 | 51.7 |

| Pre-stripping | – | 46.8 | – |

| Leach pad | 14.7 | 12.4 | 49.8 |

| ADR plant | 11.0 | 6.6 | – |

| Mill CIL | – | 42.3 | – |

| Facilities, support and infrastructure | 7.8 | 24.1 | – |

| Plant mobile equipment | 1.1 | 4.6 | 7.0 |

| EPCM | 0.6 | 11.2 | 2.0 |

| Owner’s costs | 5.3 | 2.5 | – |

| Construction indirects | 1.6 | 2.6 | 2.0 |

| Working capital | 3.8 | 13.9 | – |

| Contingency | 4.3 | 16.5 | 9.4 |

| Closure | – | – | 20.2 |

| Total | $51.7 | $295.0 | $142.0 |

Castle Mountain Operating Cost Estimates

| Phase 1 | Phase 2 | Total Project | ||||

| $/oz | $/t | $/oz | $/t | $/oz | $/t | |

| Mining ($/ mined) | 1.84 | 1.37 | 1.39 | |||

| Mining ($/ processed) | 514 | 4.01 | 447 | 6.61 | 450 | 6.38 |

| Processing ($/ processed) | 220 | 1.72 | 146 | 2.15 | 149 | 2.11 |

| G&A ($/ processed) | 120 | 0.94 | 53 | 0.78 | 56 | 0.80 |

| Total onsite costs | 854 | 646 | 656 | |||

| Refining, transport | 2 | 2 | 2 | |||

| Total cash costs | 855 | 648 | 658 | |||

| Royalties | 34 | 55 | 54 | |||

| Total cash costs | 889 | 703 | 712 | |||

| Sustaining capex | 91 | 42 | 44 | |||

| Mine closure | – | 8 | 7 | |||

| AISC | $980 | $752 | $763 |

Notes: Numbers may not sum due to rounding.

MINERAL RESERVES & RESOURCES

Proven and Probable Mineral Reserves are estimated at 3.6 million oz of gold contained in 197.6 million tonnes of ore at a diluted gold grade of 0.56 g/t. These Mineral Reserves support an initial 16-year mine life with potential to expand the reserve base and extend the mine life with exploration success.

The combined Measured & Indicated Mineral Resources are estimated at 4.3 million oz of gold (inclusive of reserves) with 3.0 million oz in the Measured category contained in 160.6 million tonnes at a gold grade of 0.58 g/t and 1.3 million oz in the Indicated category contained in 81.4 million tonnes at a gold grade of 0.51 g/t, and additional Inferred Mineral Resources of 2.2 million oz contained in 171.4 million tonnes at a gold grade of 0.40 g/t.

Castle Mountain Mineral Reserve Estimate

Effective Date June 29, 2018

| Proven | Probable | Proven & Probable | |||||||

| Resource Area | Tonnes (M) | Grade (g/t) | Contained Gold (Moz) | Tonnes (M) | Grade (g/t) | Contained Gold (Moz) | Tonnes (M) | Grade (g/t) | Contained Gold (Moz) |

| JSLA – Rock | 56.7 | 0.52 | 0.95 | 1.7 | 0.92 | 0.05 | 58.5 | 0.54 | 1.01 |

| JSLA – Pit fill | 16.3 | 0.35 | 0.18 | 16.3 | 0.35 | 0.18 | |||

| Jumbo | 8.9 | 0.77 | 0.22 | 2.6 | 0.39 | 0.03 | 11.5 | 0.68 | 0.25 |

| Oro Belle | 38.7 | 0.57 | 0.71 | 6.2 | 0.48 | 0.10 | 45.0 | 0.56 | 0.80 |

| East Ridge | 5.1 | 0.80 | 0.13 | 6.4 | 0.42 | 0.09 | 11.6 | 0.59 | 0.22 |

| South Domes | 27.1 | 0.63 | 0.55 | 27.7 | 0.62 | 0.56 | 54.8 | 0.63 | 1.10 |

| Total | 136.6 | 0.58 | 2.56 | 61.0 | 0.51 | 1.00 | 197.6 | 0.56 | 3.56 |

Notes: The Mineral Reserve estimate with an effective date of June 29, 2018 is based on the Mineral Resource estimate with an effective date of March 29, 2018 that was prepared by Don Tschabrun, SME RM of Mine Technical Services. The Mineral Reserve was estimated by Global Resource Engineering, LLC with supervision by Terre Lane, MMSA, SME RM. Mineral Reserves are estimated within the final designed pit which is based on the $850/oz pit shell with a gold price of $1,250/oz. The minimum cut-off grade was 0.14 g/t gold and 0.17 g/t gold for Phases 1 and 2, respectively. Average life of mine costs are $1.39/tonne mining, $2.11/tonne processing, and $0.80/tonne processed G&A. The average process recovery was 72.4% for ROM and 94% for Mill/CIL. Tonnes and gold ounces are both reported in millions. Small differences in total tonnage and grade may occur due to rounding. The Mineral Resource estimate is inclusive of Mineral Reserves.

Drilling at Castle Mountain in 2017 identified a new zone of significant near-surface mineralization at the East Ridge target, peripheral to the current resource pit, with grades significantly higher than the current resource grade. Exploration also identified some higher-grade intercepts at depth in the JSLA Pit that could pull the current pit bottom lower and expand the defined resource boundary at depth. Equinox Gold intends to continue drilling at Castle Mountain with the objective of extending the mine life and potentially bringing higher-grade, near-surface mineralization into the mine plan to increase annual production and reduce the LOM strip ratio.

CASTLE MOUNTAIN MINE PLAN

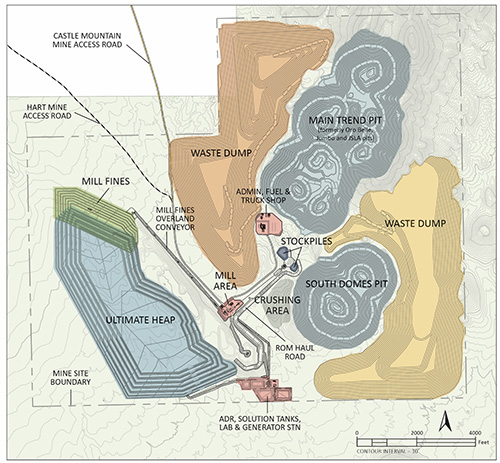

During previous operations, material below 0.5 g/t gold mined from the Oro Belle and Jumbo pits was placed into the JSLA Pit (Figure 1). Phase 1 ore will be sourced primarily from this stockpile of lower-grade material, which will be placed on the heap leach pad in 15-metre lifts at a rate of 12,700 tpd and leached. Average annual production during Phase 1 is estimated at 45,000 oz of gold for total Phase 1 production of 135,000 oz of gold.

Phase 2, treating ore mined from the large Main Trend and South Domes pits (Figure 1), comprises two circuits whereby an average of 38,600 tpd of ore grading between 0.17 g/t gold and 1.3 g/t gold will be placed directly on the ROM heap leach pad and ore above the 1.3 g/t cut-off will be milled and processed via a CIL (carbon-in-leach) circuit at an average rate of 2,400 tpd. Average annual production during Phase 2 is estimated at 203,000 oz of gold for total anticipated production from Phase 2 of 2.7 million oz of gold. The operating plan calls for 5% of the ore tonnes, containing 29% of LOM produced gold, to be processed by CIL.

Metallurgical test work shows average recoveries of 72% for ROM operations and 94% for milling operations, with average LOM recoveries of 79%.

Mine design and preparation of the mining reserves was completed using conventional open-pit design practice. The designs are based on the $850/oz Lerchs-Grosmann optimal pit solution. From that initial pit design, ramp systems were designed and the pits were divided into 14 different laybacks/phases. Mining of the pits was subsequently scheduled to provide the required ore per year in the plan while balancing the waste mining to ensure proper development of the Project.

During the first two years of operations mining will be performed exclusively by a mining contractor. In years 3 and 4 the mining contractor will continue mining and will also assist with pre-stripping operations, which will be primarily undertaken by the Company’s own mining fleet. Contract mining operations will cease by year 5. Grade control will be performed by Castle Mountain personnel throughout the mine life.

It is anticipated that the mining contractor will use a fleet of 85-tonne to 100-tonne capacity rear dump trucks and equivalent class front-end-loaders. The initial owner fleet is expected to comprise 17 180-tonne capacity rear dump trucks and four 425-tonne class excavators. Mining will take place on 6.1-metre (20 foot) benches, with double benching anticipated in waste areas.

Mining costs are estimated at $1.39 per tonne mined over the current LOM.

Figure 1 – Castle Mountain Site Plan

PROCESSING

Phase 1 processing operations will treat the solutions from the ROM heap leach facility operating in a new ADR (adsorption, desorption and refining) plant capable of treating 400 cubic metres per hour (“m3/hr”) of pregnant solution to produce doré bars.

Phase 2 will require an expansion of the solution handling and ADR plant capacity to receive the additional flow from the increased ROM heap leaching operations and loaded carbon from the CIL plant. The Phase 2 CIL circuit will comprise a three-stage crushing circuit, ball mill, a gravity circuit, a CIL circuit, an Acacia high intensity leach circuit, a cyanide destruction circuit, and a mill fines filtration circuit. The comminution circuit is designed to achieve 80% passing 150 microns. Loaded carbon from the CIL circuit will be treated in ROM desorption and recovery circuits. The expanded plant will have capacity to treat 1,900 m3/hr to produce doré bars.

Processing costs are estimated at $2.11 per tonne treated over the current LOM.

HEAP LEACH PADS

The heap leach pads for both phases will be double synthetic lined using 2.0 mm LLDPE liner with a leak detection and recovery system between the synthetic liners. Spent heap leach ore from prior operations will be used to form a 600 mm drainage layer above the lining system. Ore will be stacked in 15-metre lifts with no inter-lift liners. Heap irrigation, at a nominal rate of 10 l/hr/m2, will be delivered via buried drip lines to reduce evaporative losses of solution. Leaching reagent consumptions are expected to be 0.1 kg/t NaCN and 1.2 kg/t lime.

POWER

Power for Phase 1 operations will be provided from on-site propane generators. Power for Phase 2 operations will be obtained from a substation in the nearby town of Searchlight, Nevada and delivered via a 69kV powerline that will be constructed for Phase 2 operations.

WATER

Phase 1 operations require approximately 23 litres per second (“l/s”) of water that will be provided from existing water wells at the Project. Phase 2 operations require approximately 60 l/s of water that the Company expects to source from existing water wells and from additional nearby water sources.

WASTE DUMPS, BACKFILL & MILL FINES DISPOSAL

Over the LOM, 58% of the mine waste will be placed in waste dumps to the SE and NW of the active mining areas and the 42% balance will be placed as backfill in the Main Trend Pit.

Approximately 10.7 million tonnes of mill fines will be treated to remove cyanide using a Caro’s acid system, filtered, and then dry stacked at the north end of the heap leach pad. The mill fines will be stacked on the same lining system as the ROM heap leach material (double synthetic liner) and isolated from the ROM heap leach material by an intermediate liner on the interface between the ROM material and the fines.

LABOUR AND SUPPLIES

The Project is approximately a 1.3-hour drive south from Las Vegas, Nevada and accessible year-round by paved highways and well-maintained gravel roads. Construction and operations personnel will be stationed in nearby communities without the need for an on-site camp. There is abundant skilled labour in the region and the Project will provide up to 600 jobs during both construction and operations. The Project is located in the southwest United States mining district and a number of major mining suppliers have distribution hubs in the region.

PERMITTING

The Company has maintained its permits in good standing since prior operations ceased and has the key permits required to commence Phase 1 production including a San Bernardino County CUP and a Federal ROD. Certain administrative State permits are required for Phase 1 and are expected to be received in early to mid-2019.

To permit Phase 2, with a higher processing rate, increased water consumption and a larger area of impact, the Company will modify its existing plan of operations and permits. None of the flora and fauna surveys and environmental studies to date have identified material changes to the mine area compared to the area during previous operations. The Company intends to submit its updated mine plan and reclamation plan by mid-2019 with the target of commencing Phase 2 construction upon receipt of permits.

NEXT STEPS & TIMELINES

The Company intends to advance Phase 1 basic engineering with the target of stacking ore on the heap leach pad and commissioning the ADR plant in late 2019. Concurrently, the Company will undertake a feasibility study and permitting to support development of Phase 2. Data collection for Phase 2 permitting is underway. The Company is also in the process of permitting a water well development program.

TECHNICAL REPORT PREPARATION

The PFS was prepared by several independent Qualified Persons (“QPs”) and was consolidated by Kappes Cassiday & Associates (“KCA”), supported by Mine Technical Services (“MTS”), Global Resource Engineering (“GRE”), Call & Nicholas (“CNI”), Geo-Logic Associates (“GLA”) and Lilburn Corporation. The Mineral Resources were prepared by MTS based on the geological model prepared by Equinox Gold geologists, which MTS reviewed and agreed when preparing the block model. The Mineral Reserves, mine plan and mining sections of the study were prepared by GRE, the mine geotechnical section was prepared by CNI and environmental matters were led by San Bernardino-based Lilburn Corporation. The heap leach pad and hydrogeology aspects of the study were prepared by GLA. The PFS is being summarized into a technical report that will be filed on SEDAR within 45 days, in accordance with National Instrument 43-101 (“NI 43-101”).

CONFERENCE CALL / WEBCAST

The Company will host a webcast and conference call on July 17, 2018 to present the Castle Mountain PFS results. The webcast and presentation slides will also be archived and accessible on Equinox Gold’s website. Please register five to 10 minutes before the scheduled start time and ask to join the Equinox Gold call.

Tuesday, July 17, 2018 at 8:00am Pacific Time (11:00am Eastern Time)

Toll-free in U.S. and Canada: 1-800-319-4610

International callers: +1 604-638-5340

Login to the webcast

QUALIFIED PERSONS

The technical content of this press release has been reviewed and approved by the QPs who were involved with preparation of the PFS: Tim Scott, SME RM of KCA; Todd Wakefield, SME RM of MTS; Don Tschabrun, SME RM of MTS; Terre Lane, MMSA, SME RM of GRE; Ross Barkley, PE of CNI; and Monte Christie, PE, GE of GLA. David Laing, BSc, MIMMM, Equinox Gold’s COO, and Marc Leduc, P.Eng., Equinox Gold’s EVP US Operations, are QPs under NI 43-101 and have also reviewed, approved and verified the technical content of this news release.

For readers to fully understand the information in this release they should read the technical report in its entirety when it is available on SEDAR, including all qualifications, assumptions, exclusions and risks that relate to the PFS. The technical report is intended to be read as a whole and sections should not be read or relied upon out of context.

CAUTIONARY NOTES AND FORWARD-LOOKING STATEMENTS

Neither the TSX Venture Exchange nor its Regulation Services Provider (as such term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Aurizona Gold Mine Reserve Estimate

This document makes reference to the Mineral Reserve Estimate for Equinox Gold’s Aurizona Gold Mine in Brazil. The Aurizona Mineral Reserve estimate has an effective date of May 29, 2017 and was reported in the “Feasibility Study on the Aurizona Gold Mine Project” prepared by Lycopodium Minerals Canada Ltd. with an effective date of July 10, 2017, which is available for download on the Company’s website and on SEDAR at www.sedar.com. The combined Proven & Probable Mineral Reserves at Aurizona are estimated at 971,000 oz of gold contained in 19.8 million tonnes at a gold grade of 1.52 g/t, with 392,000 oz in the Proven category contained in 8.4 million tonnes at a gold grade of 1.44 g/t and 579,000 oz in the Probable category contained in 11.4 million tonnes at a gold grade of 1.58 g/t.

Forward-looking Statements

This document contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). The use of the words “contemplates”, “generate”, “will”, “developed”, “potential”, “objective”, “plan”, “enhance”, “completing”, “could”, “intends”, “potentially”, “anticipated”, “expects”, “target”, and similar expressions are intended to identify forward-looking statements. Forward-looking statements contained in this press release include statements regarding planned development activities, planned environmental and engineering studies, completion and filing of the prefeasibility study, completion of a feasibility study and the results of the study, the anticipated restart of production at Castle Mountain, and the anticipated capital costs, sustaining costs, net present value, internal rate of return, availability of labour, gold recoveries, production rates, tax rates and commodity prices that would support redevelopment of Castle Mountain, and the anticipated restart of production at Aurizona. Information concerning mineral re/_modules/bCMS/content/forms/source/reserve estimates and the economic analysis thereof contained in the results of the Castle Mountain prefeasibility study are also forward-looking statements in that they reflect a prediction of the mineralization that would be encountered, and the results of mining, if a mineral deposit were developed and mined. Although Equinox Gold believes that the expectations reflected in such forward-looking statements and/or information are reasonable, undue reliance should not be placed on forward-looking statements since Equinox Gold can give no assurance that such expectations will prove to be correct. These statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking statements, including the risks, uncertainties and other factors identified in Equinox Gold’s periodic filings with Canadian securities regulators, and assumptions made with regard to the Company’s ability to complete a feasibility study for Castle Mountain and to achieve the results outlined in the feasibility study; the anticipated Board of Directors decision to approve construction of Castle Mountain; the ability to raise the capital required to fund construction and development of Castle Mountain; the ability to restart production at Castle Mountain; timing of the anticipated restart of production; and the results and impact of future exploration at Castle Mountain. Furthermore, the forward-looking statements contained in this news release are made as at the date of this news release and Equinox Gold does not undertake any obligations to publicly update and/or revise any of the included forward-looking statements, whether as a result of additional information, future events and/or otherwise, except as may be required by applicable securities laws.

Estimates of Measured, Indicated and Inferred Mineral Resources

Information regarding reserve and resource estimates has been prepared in accordance with Canadian standards under applicable Canadian securities laws, and may not be comparable to similar information for United States companies. The terms “Mineral Resource”, “Measured Mineral Resource”, “Indicated Mineral Resource” and “Inferred Mineral Resource” used in this news release are Canadian mining terms as defined in accordance with NI 43-101 under guidelines set out in the Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”) Standards on Mineral Resources and Mineral Reserves adopted by the CIM Council on May 10, 2014. While the terms “Mineral Resource”, “Measured Mineral Resource”, “Indicated Mineral Resource” and “Inferred Mineral Resource” are recognized and required by Canadian regulations, they are not defined terms under standards of the United States Securities and Exchange Commission. Under United States standards, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve calculation is made. As such, certain information contained in this news release concerning descriptions of mineralization and resources under Canadian standards is not comparable to similar information made public by United States companies subject to the reporting and disclosure requirements of the United States Securities and Exchange Commission. An “Inferred Mineral Resource” has a great amount of uncertainty as to its existence and as to its economic and legal feasibility. It cannot be assumed that all or any part of an “Inferred Mineral Resource“ will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of feasibility or other economic studies. Readers are cautioned not to assume that all or any part of Measured or Indicated Resources will ever be converted into Mineral Reserves. Readers are also cautioned not to assume that all or any part of an “Inferred Mineral Resource” exists or is economically or legally mineable. In addition, the definitions of “Proven Mineral Reserves” and “Probable Mineral Reserves” under CIM standards differ in certain respects from the standards of the United States Securities and Exchange Commission.