Released on

Equinox Gold Announces Positive Feasibility Study for Castle Mountain Phase 2 Expansion: Average Annual Phase 2 Production of 218,000 oz of Gold, After-tax NPV5% of $640 Million and IRR of 18% at $1,500/oz Gold

Download PDFAll dollar figures in US dollars, unless otherwise indicated

Equinox Gold Corp. (TSX: EQX, NYSE American: EQX) (“Equinox Gold” or the “Company”) is pleased to announce the results of a Feasibility Study (“2021 Feasibility”) for the Phase 2 expansion (“Phase 2”) at the Company’s 100%-owned Castle Mountain Gold Mine (“Castle Mountain”) located in California, USA. On a standalone basis, Phase 2 is expected to produce 3.2 million ounces (“oz”) of gold at average all-in-sustaining costs (“AISC”) of $858 per oz of gold sold. Using the base case $1,500/oz gold price, Phase 2 has an after-tax net present value of $640 million (“NPV5%” discounted at 5% from the start of Phase 2 construction) and an internal rate of return (“IRR”) of 18%.

Castle Mountain achieved Phase 1 commercial production in November 2020, with expected production of 30,000 to 40,000 oz of gold annually. The current operation consists of a run-of-mine (“ROM”) heap leach facility placing 12,700 tonnes of ore per day (“t/d”). Phase 2 will expand ROM heap leaching and incorporate milling of higher-grade ore, increasing production to an average of 218,000 oz per year for 14 years followed by leach pad rinsing to recover residual gold. Life-of-mine production including Phase 1 operations and end of mine life rinsing is estimated at 3.4 million oz of gold.

PHASE 2 EXPANSION HIGHLIGHTS (Phase 2 only at base case $1,500/oz gold, unless otherwise indicated)

- After-tax NPV5% of $640 million ($1.1 billion at $1,800/oz gold)

- After-tax IRR of 18% (25% at $1,800/oz gold)

-

$1.3 billion after-tax cumulative net cash flow ($2.0 billion at $1,800/oz gold)

- $114.1 million average annual after-tax net cash flow ($161.8 million at $1,800/oz gold)

- $806/oz average cash costs

- $858/oz average AISC

- 218,000 oz average annual gold production

-

3.2 million oz total gold production at an overall average recovery of 82%

- 1.1 million oz produced from the mill at an average recovery of 94%

- 2.1 million oz produced from the heap leach at an average recovery of 67% (74% after final rinsing)

-

$389 million initial capital costs, excluding $121 million leased mining fleet

- $510 million if the fleet is purchased up front; NPV5% and IRR assume fleet is purchased up front

- $147 million sustaining capital costs over the Phase 2 mine life

- 14-year Phase 2 mine life with expansion potential from exploration, plus two to three years of residual leaching and final rinsing

-

Total life-of-mine project, including both Phase 1 and Phase 2 operations

- 3.4 million oz gold production

- 4.2 million oz of Proven and Probable Mineral Reserves grading 0.51 grams per tonne (“g/t”) gold

- 1.5 million oz of Measured & Indicated Mineral Resources (exclusive of Reserves) grading 0.62 g/t gold

Christian Milau, CEO of Equinox Gold, stated: “The Castle Mountain Phase 2 expansion will increase production from the mine to well over 200,000 ounces of low-cost annual gold production and generate nearly $2 billion of net cash flow at current gold prices. Phase 2 will also provide more than 400 jobs during construction and operations and extend the total mine life to more than 20 years. With Phase 1 in operations and Phase 2 permitting underway, Castle Mountain will be a significant economic driver in the region and a long-life cornerstone asset for Equinox Gold.”

OVERVIEW

The Castle Mountain Gold Mine, located in San Bernardino County, California, produced more than one million oz of gold as an open-pit heap leach mine from 1992 to 2004, when production ceased due to low gold prices and the mine was substantially reclaimed. Equinox Gold completed Phase 1 construction in September 2020 with no lost-time injuries and achieved Phase 1 commercial production on November 21, 2020.

The 2021 Feasibility outlines an expansion of the mine that will include a 45,350 t/d ROM heap leach facility and a new 3,200 t/d milling and leach/carbon-in-leach (“CIL”) plant for higher grade ore. The existing open pits will ultimately join to become the Main Pit which, with the South Domes Pit, will provide Phase 2 ore.

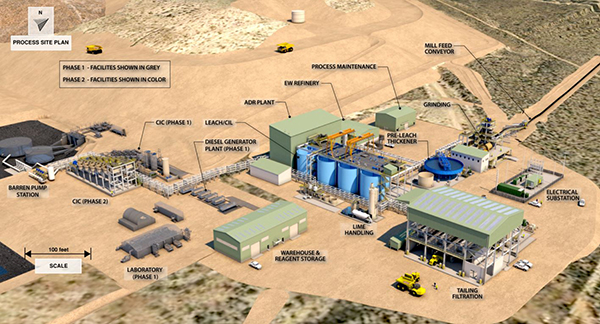

PROCESS PLANT AND PROJECT INFRASTRUCTURE

Phase 2 will operate within the current approved Mine Permit boundary and existing site infrastructure will be incorporated into Phase 2, including administration buildings, haul roads, solution handling pumps and storage tanks, a carbon-in-column (“CIC”) plant, a cyanide receiving and storage area, a lined event pond, a diesel power generation plant and an assay and metallurgical laboratory.

Castle Mountain Overall Site Plan

The Phase 2 heap leach facility will consist of an enlarged heap leach pad, an additional event pond, additional larger solution handling pumps and an additional CIC plant. The new mill facility will consist of a two-stage crushing facility, conveyors, ball mill circuit, gravity concentration, leach and CIL tanks, thickeners, filters and a reagent handling area. Loaded carbon will be processed in a desorption, electrowinning and refinery plant. Additional infrastructure for Phase 2 includes water supply wells, pumps and distribution systems, installation of an electrical transmission line along a previous corridor, an electrical substation, a filtered tailings storage facility, an extension of two waste rock dumps, a truck shop, and various site improvements and upgrades to meet the expanded project needs.

CAPITAL AND OPERATING COSTS

The 2021 Feasibility contemplates a two-year construction timeline. Total initial capital costs are estimated at $389 million, excluding $121 million for a leased mining fleet, or a total of $510 million if the fleet is purchased up front. All economics below are based on the assumption that the mining fleet is purchased up front.

Sustaining capital costs of $147 million are primarily for mine equipment and development of additional stages of the heap leach pad and filtered tailings facilities, plus additional closure costs of $22 million at the end of the mine life.

Castle Mountain Capital Costs

| Item | Initial ($M) | Sustaining ($M) | Total ($M) |

| Mine Equipment1 | 154 | 70 | 224 |

| Mine Development | 41 | 11 | 52 |

| Mine Total | 195 | 81 | 276 |

| General Siteworks | 11 | – | 11 |

| Heap Leach and Solution Handling | 38 | 56 | 94 |

| Process Plant | 62 | – | 62 |

| Tailings Filtration and Storage | 16 | 1 | 17 |

| Infrastructure | 41 | – | 41 |

| Freight | 8 | – | 8 |

| EPCM, Vendor Support and Other Indirects | 51 | – | 51 |

| Transmission Line | 15 | – | 15 |

| Owner’s Cost, Working Cap and Taxes | 40 | – | 40 |

| Total Plant and Infrastructure | 282 | 57 | 339 |

| Contingency | 33 | 9 | 42 |

| Total Capital | $510 | $147 | $657 |

| Less Leased Mining Equipment | (121) | – | (121) |

| Total Capital with Leased Equipment | $389 | – | $536 |

1. Mine equipment includes sales tax.

Operating costs for Phase 2 are estimated at $10.27 per tonne of ore processed, as summarized below. Cash costs are estimated at $806/oz with AISC estimated at $858/oz of gold sold.

Castle Mountain Operating Costs

| Total Operating Costs | $/tonne |

| Mining ($/mined) | 1.93 |

| Mining ($/processed) | 6.83 |

| Processing – ROM heap leach Processing – Milled Processing Total ($/processed) | 1.71 15.85 2.70 |

| G&A ($/processed) | 0.72 |

| Refining and Transportation | 0.02 |

| Total | $10.27 |

Castle Mountain Operating Costs

| Item | Total Cost ($M) | Unit Cost ($/oz) |

| Mining | 1,567 | 490 |

| Processing – Heap Leach | 365 | 115 |

| Processing – Mill/CIL | 255 | 80 |

| G&A | 164 | 51 |

| Operating Cost | 2,351 | 736 |

| Royalties | 214 | 67 |

| Refining and Transportation | 5 | 2 |

| Adjusted Operating Cost | 2,570 | 806 |

| Sustaining Capital | 147 | 46 |

| Salvage Value | (3) | – |

| Reclamation and Closure | 22 | 7 |

| AISC | $2,736 | $858 |

ECONOMIC SENSITIVITIES

Using the base case gold price of $1,500/oz and incorporating only Proven and Probable Mineral Reserves, the Project has an after-tax NPV5% of $640 million and an after-tax IRR of 18%. Project economics are most sensitive to overall operating cost and changes in the gold price.

Castle Mountain Sensitivity to Gold Price

| Gold price ($/oz) | $1,200 | $1,350 | $1,500 | $1,650 | $1,800 | $2,000 |

| NPV5% (after tax) | $143 M | $394 M | $640 M | $875 M | $1,104 M | $1,409 M |

| IRR (after tax) | 8% | 13% | 18% | 22% | 25% | 30% |

MINERAL RESERVES & RESOURCES

The total project mine plan is based on Proven and Probable Mineral Reserves of 257.9 million tonnes (“Mt”) grading 0.514 g/t gold for 4,168,000 contained oz of gold, an increase of 17% compared to the 2018 Prefeasibility Study. Phase 1 operations, including the ramp-up to full Phase 2 production, is expected to mine approximately 28.8 Mt of the project’s Mineral Reserves.

Castle Mountain Mineral Reserve Estimate

Effective Date June 30, 2020

| Category of Mineral Reserve | Tonnes (kt) | Gold Grade (g/t) | Contained Gold (koz) |

| Proven | 84,910 | 0.55 | 1,498 |

| Probable | 172,990 | 0.48 | 2,670 |

| Total Proven & Probable | 257,900 | 0.51 | 4,168 |

Notes: CIM Definition Standards (2014) were followed for calculating Mineral Reserves. The Mineral Reserve estimate is based upon the Mineral Resource estimate prepared for Equinox Gold Castle Mountain Venture by Trevor Rabb P.Geo, with an effective date of June 30, 2020. The Mineral Reserve was estimated by Nilsson Mine Services Ltd. with supervision by John Nilsson P.Eng. who is a Qualified Person as defined under NI 43-101. Mineral Reserves are reported within the ultimate reserve pit design with overall economics developed for $1,350/oz gold with appropriate royalties applied. Mineral Reserves are reported using a cut-off grade of 0.17 g/t gold. The mining costs average $1.78/ton ($1.96/t) mined, processing costs are $1.33/ton ($1.47/t) for ROM and $12.62/ton ($13.91/t) for milling. G&A was $0.72/ton ($0.79/t) ore processed. The average process recovery was 73.9% for ROM and 94.5% for milling. Totals may not add due to rounding.

Castle Mountain Mineral Resource Estimate (exclusive of Reserves)

Effective Date June 30, 2020

| Category of Mineral Resource | Tonnes (kt) | Gold Grade (g/t) | Contained Gold (koz) |

| Measured | 781 | 0.68 | 17 |

| Indicated | 73,452 | 0.62 | 1,453 |

| Total Measured & Indicated | 74,233 | 0.62 | 1,470 |

| Inferred | 69,890 | 0.63 | 1,422 |

Notes: CIM Definition Standards (2014) were followed for calculating Mineral Resources. The Mineral Resource statement has been prepared by Trevor Rabb, P.Geo. (Equity) who is a Qualified Person as defined by NI 43-101. Mineral Resources are reported exclusive of reserves. Mineral Resources are reported using a gold price of $1,500/oz. Open-pit Mineral Resources are reported using a cut-off grade of 0.17 g/t gold and are constrained using an optimized pit generated using Lerchs Grossmann pit optimization algorithm. Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability. Totals may not add due to rounding.

PHASE 2 EXPANSION MINE PLAN

Phase 2 will be a conventional off-road truck and shovel open-pit mining operation. As outlined in the Transition Plan table below, the 2021 Feasibility contemplates the commencement of Phase 2 pre-strip in Year 4 of the current operations and a transition to operator owned mining services prior to Year 5. Phase 2 mining production will ramp-up in Year 5 with full Phase 2 mining production coinciding with the start of the fully expanded processing facilities, estimated to be at the start of Year 6.

The Phase 2 mine plan outlines nine phases of open-pit mining from five pit areas – JSLA (3 phases), Jumbo, Oro Belle, East Ridge (2 phases) and South Domes (2 phases) – starting with JSLA backfill and moving north, and then to South Domes to complete the operation. The mining sequence of the phases allows for backfilling of waste as the pit reaches final limits.

The Phase 2 mine production schedule delivers 213.4 Mt of ore grading 0.41 g/t gold to the ROM heap leach and 16.1 Mt of ore grading 2.3 g/t gold to the mill. Waste tonnage totaling 581.7 Mt will be placed in the waste rock dumps. The Phase 2 stripping ratio is 2.54:1. Mining costs for Phase 2 are estimated to average $1.93/t mined.

Phase 1 to Phase 2 Transition Plan

| Operational Phase | Production Year | Phase 2 Expansion | Ore Mined (kt) | Gold Produced (koz) |

| Phase 1 | 1 | -5 | 4,700 | 36 |

| Phase 1 | 2 | -4 | 4,700 | 32 |

| Phase 1 | 3 | -3 | 4,700 | 29 |

| Phase 1 + Phase 2 Pre-strip | 4 | -2 | 4,700 | 28 |

| Phase 1 to 2 Ramp-up | 5 | -1 | 10,100 | 63 |

| Phase 2 | 6 | 1 | 17,500 | 203 |

| Phase 2 + Start of Rinsing | 7-19 | 2-14 | 211,600 | 2,849 |

| Phase 2 Final Rinsing | 20-21 | 15-16 | 151 | |

| Subtotal Phase 2 | 229,100 | 3,203 | ||

| Total Phase 1 + Phase 2 | 257,900 | 3,392 |

PRODUCTION SCHEDULE

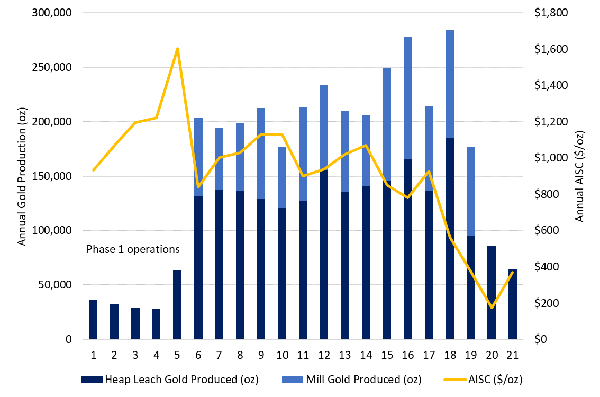

The Phase 2 production schedule shows average annual production of 218,000 oz of gold during the 14-year mine life with an average AISC of $858/oz. After mining ceases, the 2021 Feasibility anticipates two to three years of heap leach rinsing to recover residual ounces, for total production of 3,203,000 oz of gold.

Of the total annual average production of 218,000 oz per year, the mill is expected to produce an average of 79,000 oz of gold per year for total production from the mill of 1,108,000 oz of gold, with average recoveries estimated at 94%. The heap leach pad is expected to produce an average of 139,000 oz of gold per year for 14 years until the end of mine life. Residual leaching and final rinsing will produce another 246,000 ounces over three years, for total Phase 2 production from the heap leach pad of 2,095,000 oz of gold, with average recoveries estimated at 74%, after rinsing.

Castle Mountain Annual Gold Production and AISC

METALLURGY AND PROCESSING

ROM heap leach ore will be stacked in 25 ft (8 m) lifts on the heap leach pad to be leached with a dilute cyanide solution using a drip irrigation system for 80 days. After percolating through the ore, the pregnant solution will flow by gravity to a pregnant solution tank where it is pumped to a 12,000 gallons per minute (“gpm”) CIC circuit to recover the gold from solution. The carbon adsorption circuit will consist of two trains of five cascading carbon columns.

Mill ore will be dumped on a storage pad for recovery by a front-end loader and fed to a two-stage crushing plant. A batch gravity concentrator will treat a portion of the grinding circuit circulating load to recover any gravity recoverable gold with the concentrate being processed in a batch intensive leach reactor (“ILR”). Cyclone overflow will flow by gravity to a pre-leach thickener that will thicken the slurry to 45-50% solids. Thickened slurry will be pumped to a hybrid leach/CIL circuit to extract the gold.

The carbon handling circuit is designed to handle carbon from both the heap leach CIC circuit and the mill-CIL circuit in separate batch processes. The resulting pregnant solution from the carbon handling and ILR circuits will undergo electrowinning and refining to produce gold doré bars.

Leached slurry from the leach/CIL circuit will report to a cyanide recovery thickener to recycle as much water and cyanide as possible back to the process. Flocculant will be added to aid in settling solids to produce a thickened product at approximately 60% solids, which will be treated in a cyanide destruction process. The final tailings will be pressure filtered and the filter cake at approximately 18% moisture will be hauled to the filtered tailings facility where it will be stacked on the historical heap leach facility and abutted to the expanded heap leach facility, which allows the Company to minimize new land disturbances.

Castle Mountain Process Site Plan

During historical operations from 1991 to 2004, a total of 1.24 million oz of gold was recovered from 32.8 Mt of processed ore at an average grade of 1.47 g/t gold with a combined average recovery of 80% from milled and heap leached ore, and 76% recovery specifically from the heap leach ore. Metallurgical testwork completed from 2015 to 2020 on both heap leach and mill ore samples showed average gold recoveries of 80% to 82% from various column leach tests at different particle sizes, and 94% recovery from leaching milled ore.

Considering lab and historical operating data, the expected heap leach gold recovery is expected to be 67% during Phase 2 operations and 74% after final rinsing.

For mill grade ores processed through the mill with gravity concentration and a leach/CIL circuit with 30 hours of retention time, an overall gold recovery of 94% is expected.

WATER

Castle Mountain is in a semi-arid region and will be a net zero discharge facility, with most of the water loss occurring via evaporation from the surface of the heap leach pad and filtered tailings facility. Process water needs for the recovery plant will fluctuate seasonally and make-up water required for the heap leach will change with the amount of evaporation and precipitation each month. Water consumption will be mitigated using low evaporation buried drip emitters, limiting the amount of water retained in ponds with larger evaporative losses, using binders and dust collectors that limit water needs for dust suppression, and by using extensive water recycling in the process.

Annual water demand for Phase 2 is estimated to range from 1,150 gpm to 1,900 gpm depending on the season. The current water supply includes three historical wells providing approximately 150 gpm total and two recently installed wells capable of producing approximately 400 gpm total. Additional water for Phase 2 is expected to be extracted from new wells. Recent water exploration has shown very good potential for water both near site and in a neighbouring water basin. Once developed, wells in both areas are expected to produce between 500 and 1,000 gpm of water each. The Phase 2 development plans include the addition of new wells and well pumps in both locations, as well as an overland pipeline and booster pumps to meet the additional water demands.

POWER

A total of 10 MW of power is required for Phase 2 and will be provided by a connection to the grid at an existing substation near Searchlight, Nevada and routed to site via a new transmission line that will use the previous right of way established for the transmission line during historical operations. This will result in the existing diesel generators at site being re-purposed as back-up emergency electrical power.

ROYALTIES

The Project is subject to several royalties payable to different parties, with a total royalty of approximately 4.5%.

PERMITTING

The Castle Mountain Mine is located on both public and private land and historically has been permitted by co-lead agencies, the County of San Bernardino at the state level and the United States Bureau of Land Management (“BLM”) at the federal level. Castle Mountain has all permits required to conduct mining for current operations and is permitted to operate within the approved Mine Permit boundary. Phase 2 will operate within the same Mine Permit boundary; however, modifications to mine and reclamation plan elements, including increased land disturbance, mining and water extraction rates, will require updates to existing permits. Phase 2 is expected to require an updated environmental review as well as several new state and federal permits and amendments.

PROJECT DEVELOPMENT

Execution of the Castle Mountain Phase 2 expansion is expected to be completed in several stages including basic engineering or front-end engineering design (FEED), which will progress in parallel with project permitting exercises. Further stages will include detailed engineering, project construction, commissioning and project start-up and ramp-up.

The overall project timeline depends largely on attaining the discretionary operating permits from the BLM and the County of San Bernardino. Development of Phase 2 is anticipated to require an overall timeline of approximately four years from the start of permitting to achieving full expanded operations.

ADDITIONAL OPPORTUNITIES

There is considerable potential to expand Castle Mountain Mineral Resources and Mineral Reserves by exploring gold anomalies identified at East Ridge, East Flats and Egg Hill. In addition, higher gold prices could make it economic to expand the 2021 Feasibility Mineral Reserve pits and ultimately connect the JSLA and South Dome pits.

Equinox Gold is reviewing opportunities that could result in optimized land use as well as initial capital and operating cost savings. The Company has also completed and is assessing a study examining the potential to use solar power at Castle Mountain. Initial results demonstrate the solar plant levelized cost of electricity would be $0.05/kWh, compared to approximately $0.10/kWh when connected to grid electricity, for net savings per year of $1.9 million based on a capital cost of $12.8 million for a 10 MWAC photovoltaic solar plant providing 40% of the site power requirements.

TECHNICAL REPORT PREPARATION

Equinox Gold retained independent consultants to complete the 2021 Feasibility and prepare a technical report in compliance with National Instrument 43-101 (“NI 43-101”). Key aspects included in the 2021 Feasibility are further advancement on metallurgical testwork, pit design, updated mine schedule, infrastructure development, proposed expanded heap leach operations, the addition of a high-grade processing mill including filtered tailings facility, and the supporting cost development with financial model. The 2021 Feasibility includes updates to the Mineral Resource and Mineral Reserve estimates. The findings and conclusions in the 2021 Feasibility are based on information available at the time of preparation and data supplied by other consultants, as indicated in the report. The effective date of the 2021 Feasibility is February 26, 2021, which represents the date of information used in the technical report.

The Qualified Persons (“QPs”) are Gabriel Secrest, P.E. and Laurie Tahija, P.E., both of M3 Engineering and Technology Corporation; Eleanor Black, P.Geo and Trevor Rabb, P.Geo, both of Equity Exploration Consultants Ltd.; John Nilsson, P.Eng., of Nilsson Mine Services Ltd.; and Doug Bartlett, P.Geo, of Clear Creek Associates. The Mineral Resources were prepared by Trevor Rabb based on the geological model prepared by Equinox Gold geologists, which Equity Exploration Consultants reviewed and agreed when preparing the block model. The Mineral Reserves, mine plan and mining sections of the study were prepared by Nilsson Mine Services with supervision by John Nilsson. The 2021 Feasibility is being summarized into a technical report that will be filed within 45 days on the Company’s website at www.equinoxgold.com, on SEDAR at www.sedar.com and on EDGAR at www.sec.gov/edgar, in accordance with NI 43-101.

For readers to fully understand the information in this news release they should read the technical report in its entirety when it is available, including all qualifications, assumptions, exclusions and risks. The technical report is intended to be read as a whole and sections should not be read or relied upon out of context.

QUALIFIED PERSONS

The technical content of this press release has been reviewed and approved by the QPs who were involved with preparation of the 2021 Feasibility: Gabriel Secrest, Laurie Tahija, Eleanor Black, Trevor Rabb, John Nilsson and Doug Bartlett.

The technical content of this press release has also been reviewed and approved by Doug Reddy, Msc., P.Geo., Equinox Gold’s COO, Kevin Scott, P.Eng., Equinox Gold’s VP Projects, and Scott Heffernan, M.Sc., P.Geo., Equinox Gold’s EVP Exploration, all of whom are Qualified Persons under NI 43-101 for Equinox Gold.

ABOUT EQUINOX GOLD

Equinox Gold is a Canadian mining company with seven operating gold mines, construction underway at an eighth site, a multi-million-ounce gold reserve base and a clear path to achieve one million ounces of annual gold production from a pipeline of development and expansion projects. Equinox Gold operates entirely in the Americas, with two properties in the United States, one in Mexico and five in Brazil. On December 16, 2020, Equinox Gold announced its friendly acquisition of Premier Gold Mines, which will bring further diversification and scale with the addition of a producing mine in Mexico and a construction-ready project in Ontario, Canada. Equinox Gold’s common shares are listed on the TSX and the NYSE American under the trading symbol EQX. Further information about Equinox Gold’s portfolio of assets and long-term growth strategy is available at www.equinoxgold.com or by email at ir@equinoxgold.com.

CAUTIONARY NOTES AND FORWARD-LOOKING STATEMENTS

Cautionary Note to U.S. Readers Concerning Estimates of Mineral Reserves and Mineral Resources

Information about mineral reserve and resource estimates in this news release has not been prepared in accordance with the requirements of U.S. securities laws. The technical information in this news release has been prepared in accordance with Canadian reporting standards and certain estimates are made in accordance with NI 43-101. NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of technical information concerning mineral projects. Unless otherwise indicated, all mineral reserve and resource estimates contained in this news release have been prepared in accordance with NI 43-101 and the Canadian Institute of Mining, Metallurgy and Petroleum Definition Standards on Mineral Resources and Reserves (CIM Definition Standards). Canadian standards, including NI 43-101, differ significantly from the historical requirements of the Securities and Exchange Commission (the SEC), and mineral reserve and resource estimates contained in this news release, or incorporated by reference, may not be comparable to similar information disclosed by U.S. companies. The SEC has adopted amendments to its disclosure rules to modernize the mineral property disclosure requirements for issuers whose securities are registered with the SEC (the SEC Modernization Rules). The SEC Modernization Rules replace the historical property disclosure requirements for mining registrants that are included in SEC Industry Guide 7. U.S. companies must provide disclosure on mineral properties under the SEC Modernization Rules for fiscal years beginning January 1, 2021 or later. Under the SEC Modernization Rules, the definitions of proven mineral reserves and probable mineral reserves have been amended to be substantially similar to the corresponding CIM Definition Standards and the SEC has added definitions to recognize measured mineral resources, indicated mineral resources and inferred mineral resources which are also substantially similar to the corresponding CIM Definition Standards; however, there are still differences in the definitions and standards under the SEC Modernization Rules and the CIM Definition Standards. Therefore, the Company’s mineral resources and reserves as determined in accordance with NI 43-101 may be significantly different than if they had been determined in accordance with the SEC Modernization Rules.

Non-IFRS Measures

This news release refers to mine cash costs per ounce sold, all-in sustaining costs (“AISC”), and sustaining and expansion capital costs that are measures with no standardized meaning under International Financial Reporting Standards (“IFRS”) and may not be comparable to similar measures presented by other companies. Their measurement and presentation is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Non-IFRS measures are widely used in the mining industry as measurements of performance and the Company believes that they provide further transparency into costs associated with producing gold and will assist analysts, investors and other stakeholders of the Company in assessing its operating performance, its ability to generate free cash flow from current operations and its overall value. Refer to the “Non-IFRS measures” section of the Company’s Management’s Discussion and Analysis for the period ended December 31, 2020, for a more detailed discussion of these non-IFRS measures and their calculation.

Forward-looking Statements

This news release contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation and may include future-oriented financial information. Forward-looking statements and forward-looking information in this news release relate to, among other things: the Company’s ability to successfully advance the Castle Mountain Phase 2 expansion, the planned acquisition of Premier Gold and the Company’s ability to successfully integrate those assets into its portfolio, the strategic vision for the Company and expectations regarding production capabilities and future financial or operating performance, the conversion of Mineral Resources to Mineral Reserves, and the Company’s ability to successfully advance its growth and development projects and anticipated benefits arising from the same. Forward-looking statements or information generally identified by the use of the words “will”, “expected”, “expectations”, “potential”, “estimate”, “opportunity”, “additional”, and similar expressions and phrases or statements that certain actions, events or results “could”, “would” or “should”, or the negative connotation of such terms, are intended to identify forward-looking statements and information. Although the Company believes that the expectations reflected in such forward-looking statements and information are reasonable, undue reliance should not be placed on forward-looking statements since the Company can give no assurance that such expectations will prove to be correct. The Company has based these forward-looking statements and information on the Company’s current expectations and projections about future events and these assumptions include: prices for gold remaining as estimated; currency exchange rates remaining as estimated; construction and development at Castle Mountain being completed and performed in accordance with current expectations; tonnage of ore to be mined and processed; ore grades and recoveries; the timely delivery and commissioning of equipment required for the Phase 2 expansion of Castle Mountain; availability of funds for the Company’s projects and future cash requirements; capital, decommissioning and reclamation estimates; Castle Mountain Mineral Reserve and Mineral Resource estimates and the assumptions on which they are based; prices for energy inputs, labour, materials, supplies and services; no labour-related disruptions and no unplanned delays or interruptions in scheduled construction, development and production, including by blockade; all necessary permits, licenses and regulatory approvals are received in a timely manner; and the Company’s ability to comply with environmental, health and safety laws. While the Company considers these assumptions to be reasonable based on information currently available, they may prove to be incorrect. Accordingly, readers are cautioned not to put undue reliance on the forward-looking statements or information contained in this news release.

The Company cautions that forward-looking statements and information involve known and unknown risks, uncertainties and other factors that may cause actual results and developments to differ materially from those expressed or implied by such forward-looking statements and information contained in this news release and the Company has made assumptions and estimates based on or related to many of these factors. Such factors include, without limitation: fluctuations in gold prices; fluctuations in prices for energy inputs, labour, materials, supplies and services; the timely construction of the transmission line for Phase 2; the availability of sufficient water for the operation of Phase 2, fluctuations in currency markets; operational risks and hazards inherent with the business of mining (including environmental accidents and hazards, industrial accidents, equipment breakdown, unusual or unexpected geological or structural formations, cave-ins, flooding and severe weather); inadequate insurance, or inability to obtain insurance to cover these risks and hazards; employee relations; relationships with, and claims by, local communities and indigenous populations; the Company’s ability to obtain all necessary permits, licenses and regulatory approvals in a timely manner or at all; changes in laws, regulations and government practices, including environmental, export and import laws and regulations; legal restrictions relating to mining including those imposed in connection with COVID-19; risks relating to expropriation; increased competition in the mining industry; and those factors identified in the Company’s MD&A dated March 19, 2021 for the year-ended December 31, 2020 and its Annual Information Form dated May 13, 2020, which are available on SEDAR at www.sedar.com and on EDGAR at www.sec.gov/edgar. Forward-looking statements and information are designed to help readers understand management’s views as of that time with respect to future events and speak only as of the date they are made. Except as required by applicable law, the Company assumes no obligation to publicly announce the results of any change to any forward-looking statement or information contained or incorporated by reference to reflect actual results, future events or developments, changes in assumptions or changes in other factors affecting the forward-looking statements and information. If the Company updates any one or more forward-looking statements, no inference should be drawn that the Company will make additional updates with respect to those or other forward-looking statements. All forward-looking statements and information contained in this news release are expressly qualified in their entirety by this cautionary statement.